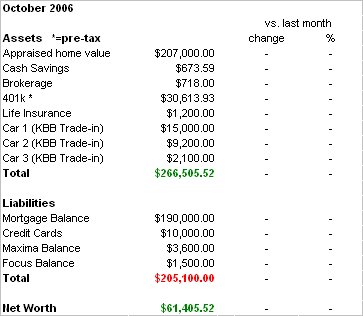

My Money Blog Goal

My 6 month goal as part of Jonathan's experiment on My Money Blog isn't off to the best start. With the new mortgage and the holidays coming up, we had to downsize our $250 per month savings into the ING Direct account to $125 per month. Along with the holidays approaching, we started the equity accelerator program through our lender, so after we make our first payment tomorrow, the next (half) payment will be coming on December 20th. I still plan on reaching my goal of $2500 by mid-May, but it's gonna take a lot of determination. Our annual bonus is up in the air as to how much it'll be, so this should be interesting. Whatever it is, I plan on saving half and using the other half toward improving our home.

Labels: Goals

posted by Jim @ 10:02 AM

1 comments

![]()

{kind=link}